What is going on with the Home Insurance Market in Myrtle Beach?

June 11, 2024, by Brad Davis, CIC

Introduction:

If you own a home in or around the Myrtle Beach area, I am sure by now you have noticed that Homeowner’s Insurance premiums have increased. You may even say the rates are going crazy.

Let’s look into some aspects of the current market, without going into all the reasons why your premium is going up. That is a topic for another blog. Although, it is important to say that premiums needed to increase. In part this is a price correction, as they were too low for years.

What are Home Insurance Companies Doing Right Now?

I am not going to give company names, but here are real examples of what some companies are doing to get back to profitability. (Some of these only apply to coastal areas.)

- Company A – Only writing new business on homes 2 years old or newer.

- Company B – Only writing new business on homes 5 years old or newer.

- Company C – Only writing new business for homes with roof 10 years old or newer.

- Company D – Only offering coverage to about 5 – 10% of applicants (declining the rest).

- Company E – Only writing new business for homes with certain wind mitigation features (almost no one qualifies).

- Company F, G, & H – Not offering any Homeowners Insurance near the coast (as they define it).

- Company I – Changing coverage for roof damage from Replacement Cost to Actual Cash Value when roof hits 10 years old.

- Company J - Changing coverage for roof damage from Replacement Cost to Actual Cash Value when roof hits 15 years old.

- Most Home Insurance Companies – Performing rigorous inspections for new business and on renewals.

- Other Home Insurance Companies – Non-renewing policies that are close to tidal water (as they define it) or to reduce their exposure in certain areas.

- Lots of Home Insurance Companies – Raising renewal premiums anywhere from 5% - 100% (with 30% being common).

What does this mean?

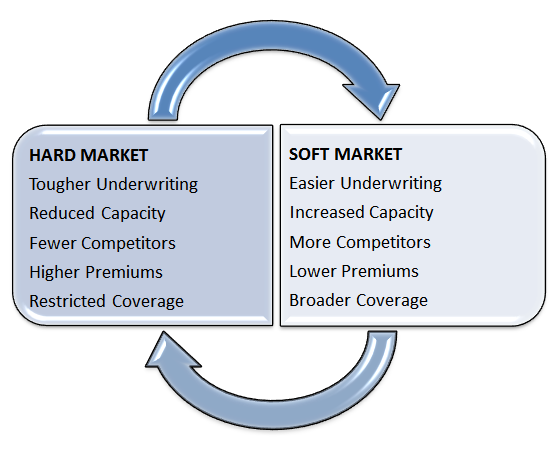

The short answer is there are less choices for home insurance today as compared to 3 years ago. This is especially true for coastal and high-risk areas (such as wildfire in California or hail in Texas).

More important than ever is the age of your roof. Insurance companies have literally gone insolvent, in part, because all the roof claims they paid over the last 5 years. Having a newer home and/or roof opens the number of companies that are willing to offer coverage. More options (competition) almost always equals finding better coverage and a lower premium.

It also means you are not alone. Practically every homeowner in Myrtle Beach has experienced an increase in their home insurance. Many have had back-to-back-to-back (3 years in a row) increases of 30%.

Final Thoughts:

When getting quotes I feel, now more than ever, it is so important to talk to a trusted insurance agent. Be cautious jumping on the lowest quote you are presented if it sounds to good to be true. The vast majority of insurance agents live up to the moral and ethical standards we have in the insurance industry, but not all have the experience needed to navigate the hard market we are in.

Lastly, sometimes you are better off to keep the policy you have. I want to give just one (of many examples) – say you find a quote that is maybe 10% cheaper than your current policy and close to your current coverages (NOTE, I did not say the same coverage because policies are NOT ALL THE SAME) and you purchase it, then the new company does their rigorous inspection and find a little damage to your roof and cancel your policy in the first 60 days. Now you go back to the company you had to find out they are not accepting new policies and cannot help you. This kind of stuff happens!

Care to see what we can do for your Home Insurance in Myrtle Beach? Please visit ThinkDavisInsurance.com or call (843)213-0000.

ThinkDavisInsurance.com

HOME | AUTO | FLOOD

We are your local independent insurance agency for Myrtle Beach providing you with peace of mind at a price that's right for you. Let Davis Insurance Associates help you find affordable home and auto insurance in South Carolina and North Carolina.